What is ESG?

ESG (environmental, social, and governance) is a framework used in investment analysis and corporate reporting of a company or organization. It helps stakeholders understand how the organization manages risks and opportunities related to issues pertaining to the environment, sustainability, and social and governance factors.

ESG is a set of environmental, social, and governance factors that companies consider when managing their business, and investors consider when investing.

Key factors and double materiality

Key ESG factors are:

- Environmental factors – the relationship between business and the natural environment (e.g., energy efficiency, greenhouse gas emissions, waste, and recycling).

- Social factors – the relationship between business and society (e.g., customer satisfaction, community investment, diversity, working conditions, and human rights).

- Governance factors – transparent, ethical and responsible management of the company (e.g., risk management, corporate governance policies and practices, transparency of reporting).

Double materiality is a concept whereby companies must consider how:

- ESG factors affect a company’s financial performance (financial materiality) – e.g., how changes in environmental legislation affect costs and revenue.

- A company’s business activities affect ESG factors (social materiality) – e.g., how production affects air pollution.

Double materiality is implemented through the identification of relevant frameworks, engagement of relevant stakeholders, categorization and assessment of factors, matrix creation, sustainability strategy development, and monitoring and reporting.

Relevant EU regulation for sustainability reporting

Investing in projects that contribute to environmental protection and climate goals is crucial within the EU. Sustainable business, financing, and reporting is a way to achieve the betterment of the planet and a green future. The EU’s goal is to implement concepts, regulations, and methodologies that will make it easier for all stakeholders to gain insight into the ESG activities of organizations.

Investing in projects that contribute to environmental protection and climate goals is crucial within the EU. Sustainable business, financing, and reporting is a way to achieve the betterment of the planet and a green future. The EU’s goal is to implement concepts, regulations, and methodologies that will make it easier for all stakeholders to gain insight into the ESG activities of organizations.

Transparent reporting and data comparison would, among other things, prevent greenwashing – a practice by which organizations only symbolically show that their activities are environmentally acceptable.

What is CSRD – Corporate Sustainability Reporting Directive?

CSRD (Corporate Sustainability Reporting Directive) is a directive that replaced NFRD (Non-Financial Reporting Directive). requires organizations to regularly and transparently report on the impact of their activities on the environment and society and on the sustainability risks to which it may be exposed. The directive aims to strengthen and standardize sustainability reporting across the EU.

Who is subject to the CSRD?

Large undertakings – exceeding 2 out of 3 criteria:

- Total assets > €25 million

- Revenue > €50 million

- Average number of employees per year > 250

The reporting obligation starts in 2028 for the financial year 2027.

Medium-sized undertakings – whose own products are placed on the EU market and do NOT exceed 2 of the 3 criteria:

- Total assets ≤ €25 million

- Revenue ≤ €50 million

- Average number of employees per year ≤ 250

The reporting obligation starts in 2029 for the financial year 2028.

Small undertakings – whose own products are placed on the EU market and do NOT exceed 2 of the 3 criteria:

- Total assets ≤ €5 million

- Revenue ≤ €10 million

- Average number of employees per year ≤ 50

The reporting obligation starts in 2029 for the financial year 2028.

Third-country undertakings – an EU subsidiary or branch whose ultimate parent company is from a third country, if:

- The subsidiary is a large enterprise or a medium/small enterprise whose own products are placed on the EU market,

- The subsidiary has a turnover of at least €40 million,

- The ultimate parent company has a turnover exceeding €150 million in the last 2 consecutive years.

The reporting obligation starts in 2029 for the financial year 2028.

CSRD in the content of the report includes the concept of double materiality, actions taken (strategy, goals, roles of the board and management and ways of determining information) and key indicators (qualitative and quantitative information).

What is the EU Taxonomy?

The EU Taxonomy is a classification system developed by the European Union to define which economic activities can be considered environmentally sustainable. The CSRD adopts the EU Taxonomy within its required report.

An environmentally sustainable activity must comply with the following:

A) it must significantly contribute to one of the following objectives:

- Climate change mitigation,

- Climate change adaptation,

- Sustainable use and protection of water and marine resources,

- Transition to a circular economy,

- Pollution prevention and control,

- Protection and restoration of biodiversity and ecosystems.

B) it must not significantly harm any of the above objectives

C) it must be carried out in accordance with minimum safeguards (harm to social and human rights must be avoided).

The required disclosures of the EU Taxonomy report are the accounting policy, taxonomy compliance assessment, and contextual information (revenue, capital, and operating expenditure).

Easy implementation of sustainability reports – SAP SCT

The aforementioned regulation poses new challenges for organizations – from data collection, to compliance with regulations and criteria, to KPI monitoring and the continuous delivery of reports.

The aforementioned regulation poses new challenges for organizations – from data collection, to compliance with regulations and criteria, to KPI monitoring and the continuous delivery of reports.

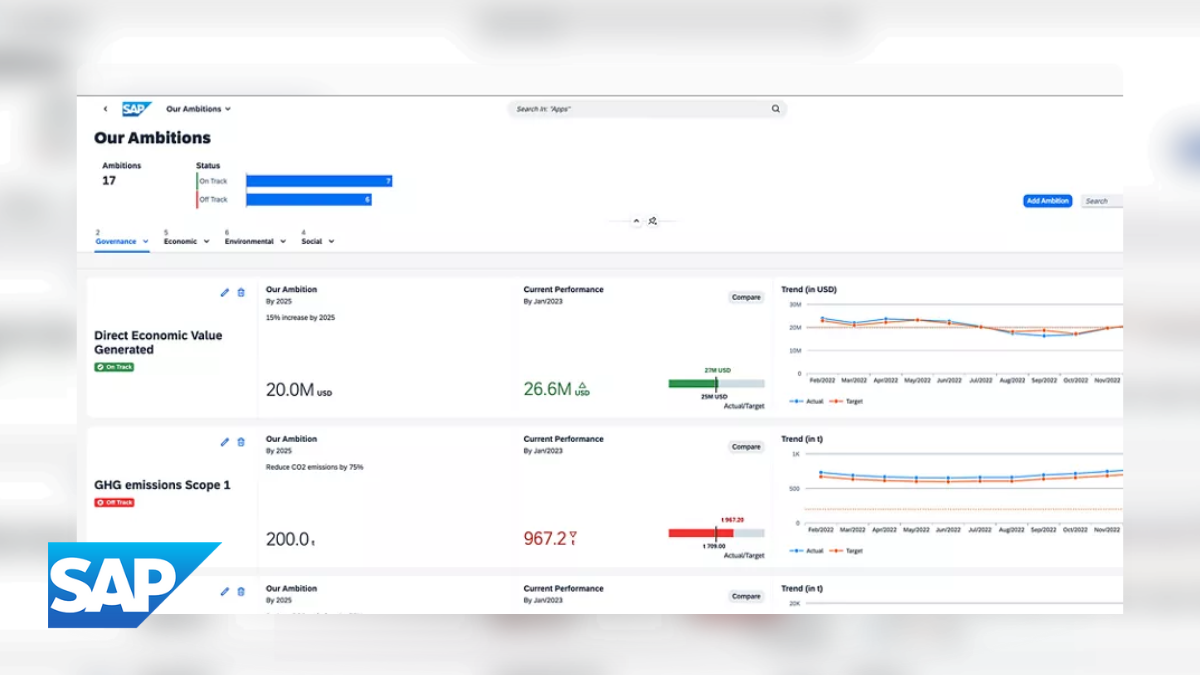

Software giant SAP has developed a solution that will help organizations simplify and speed up the reporting processes. SAP SCT (Sustainability Control Tower) is an intelligent cloud solution with which companies will be able to meet all the requirements of CSRD, EU Taxonomy, and other ESG requirements.

SAP SCT takes a key role in all steps of the process:

- Data Collection

SAP SCT can be connected to other SAP solutions and other applications via API. All necessary financial and non-financial data is in one centralized place.

It ensures data reliability and integration with the entire system.

- Reporting

SAP SCT includes ready-made report templates and metrics for CSRD, EU Taxonomy, and other ESG standards. Reporting is automated and AI-powered, eliminating the need for manual work.

Company-specific reports can also be created to facilitate audits of relevant data.

- Carrying out necessary activities

SAP SCT helps organizations monitor all activities and perform optimizations as needed. Organizations gain useful insights and can identify trends more easily and quickly, and make informed and reliable decisions.

The solution features a simple and intuitive interface suitable for all employees.

ESG and SCT as drivers of progress

SAP SCT monitors relevant EU regulations and is continuously updated to ensure that the organization is compliant with regulations. CSRD and EU Taxonomy may initially seem like regulations that impose additional obligations on businesses, but with SCT tools, they can be a competitive advantage.

Organizations can define sustainability goals, track their progress, and compare results across different business units and locations. At the same time, they can provide all relevant stakeholders with transparent insight into concrete data. SAP SCT provides reliable support for organizations in achieving sustainability goals and a green future.

If you have any questions about SAP SCT, please feel free to contact us.